Latest News

Latest News

What is 'bad bank' and can it resolve NPA woes?

Finance Minister of India has announced the formation of India’s first-ever “Bad Bank”.

- The National Asset Reconstruction Company Limited (NARCL)- India Debt Resolution Company Ltd (IDRCL) structure is the new bad bank.

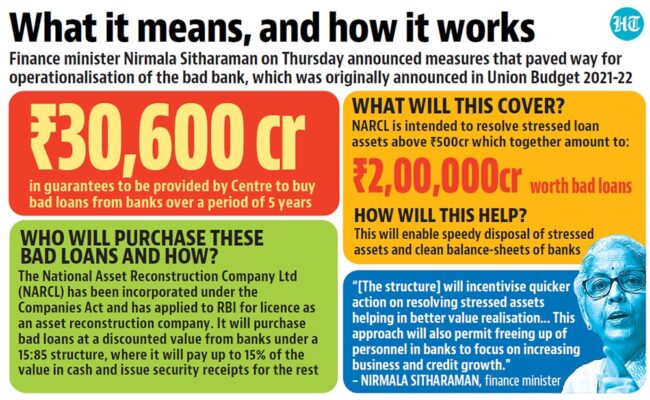

- The government has okayed the use of Rs 30,600 crore to be used as a guarantee.

- The National Asset Reconstruction Company Limited:

- It will acquire stressed assets worth about Rs 2 lakh crore from various commercial banks in different phases.

- India Debt Resolution Company Ltd (IDRCL)

- It will sell the stressed assets in the market.

Bad Bank

- A bad bank is a bank set up to buy the bad loans and other illiquid holdings of another financial institution.

- The entity holding significant nonperforming assets will sell these holdings to the bad bank at market price.

- By transferring such assets to the bad bank, the original institution may clear its balance sheet.

- If the proportion of bad loans (calculated as a percentage of the total advances) rise, then it leads to:

- The concerned bank becomes less profitable because it must use some of its profits from other loans to make up for the loss on the bad loans.

- It becomes more risk-averse.

- In India, the level of NPAs rose alarmingly since 2016. This was a result of the RBI requiring banks to clearly recognise the bad loans on their books.

The requirement of bad bank

- It was argued that the government needs to create a bad bank, an entity where all the bad loans from all the banks can be placed.

- It will reduce “stressed assets” of the commercial banks allowing them to focus on resuming normal banking operations, especially lending.

- While commercial banks resume lending, the bad bank would sell these “assets” in the market.

Working of NARCL-IDRCL

- The NARCL will first purchase bad loans from banks. It will pay 15% of the agreed price in cash and the remaining 85% will be in the form of “Security Receipts”.

- When the assets are sold, with the help of IDRCL, the commercial banks will be paid back the rest.

- If the bad bank is unable to sell the bad loan, then the government guarantee will be invoked.

- Thus, it will be paid from the Rs 30,600 crore that has been provided by the government.

Benefits of a Bad Bank

Providing Lending Leverage to Banks:- The benefits include recovered value, and significant lending leverage because of:

- Capital being freed up from less than fully provisioned bad assets.

- Capital freed up from security receipts because of a sovereign guarantee.

- Cash receipts that come back to the banks and can be leveraged for lending, also freeing up provisions from the balance sheet.

- A bad bank can help free capital of over ₹5 lakh crore that is locked in by banks as provisions against the bad loans.

POSTED ON 18-09-2021 BY ADMIN

Next previous  General Studies

General Studies

Political Science and International Relations

Some Reference Essays

List of previous year essay topics (1997-2019)

IAS GOOGLE is googled by the team of Raja Sir’s Cracking IAS Academy. Sources include The Hindu, Indian Express, pib.nic.in, Down To Earth, Economic Times, Vigyan Prasar, AIR and the like. IAS GOOGLE has been prepared in pace with emerging UPSC Trends.